Browse All Articles

<strong>Cardlytics’ State of Spend Report Shows US Spend is Highest in Four Years</strong>

ATLANTA, GA – MAY 12, 2022 – Cardlytics (NASDAQ: CDLX), an advertising platform in banks’ digital channels, today released its Q1 2022 State of Spend Report. With insight into 1 out of every 2 debit and credit card swipes in the US, Cardlytics found that overall consumer spend is up 7% in Q1 2022 versus the same quarter last year. This marks the highest consumer spending level in four years, despite concerns over record inflation.

The report, which analyzed purchase insights from the Cardlytics platform between December 30, 2021, and March 31, 2022, reveals how consumers are spending across categories including restaurant, direct-to-consumer (DTC), travel, grocery, gas, and convenience, among others. This Purchase Intelligence™ is critical for advertisers to better understand changing consumer preferences and create resulting campaigns that drive incremental returns.

A few highlights from the Q1 2022 State of Spend Report show:

- Travel and entertainment experienced significant growth (54%) as consumers began traveling again. This category led consumer spending with year-over-year (YoY) increases among airlines (99%), amusement parks (110%), concerts and theater (213%), cruise lines (345%), hotels and lodging (39%), museums and parks (55%), and travel aggregators and agencies (83%).

- Restaurant and food delivery both saw positive consumer spending. Restaurant had a 16% bump, which could be attributed partially to overall price increases. Interestingly, while restaurant delivery in Q1 increases, the overall spending for this category shows slowing growth compared to previous years (202% in 2019, 131% in 2020, 5% 2021).

- Consumers are making fewer fuel trips but are spending more per trip. As a result of the lingering effects of the pandemic, recurring supply chain roadblocks, and a recent inflation surge, gas prices have hit an all-time national average high of $4.18 per gallon. This has led to fewer, more expensive trips to the pump. The gas and convenience sector made up approximately 16.5% of customer trips in 2022, a slight decrease from 2021’s 17.3%. As oil prices increased, so did consumer purchases. In 2021, $50+ purchases were only 13% of total purchases and so far in 2022, approximately 1 in 3 fuel purchases are over $50.

- Retail spending is slowing online and in-store. While overall spending across categories is up, and in-store spending has been better than expected, consumers are starting to pull back on retail purchases. The YoY consumer spend growth for 2022 online shopping was up 44% over 2019 and up 31% over 2020. However, there was no growth in 2022 compared to 2021. For in-store shopping 2022 growth was 7% over 2019, 5% over 2020 and 3% over 2021.

“Despite supply chain challenges, ongoing pandemic uncertainty, and record-level inflation, it’s clear that consumers are continuing to spend but are also looking for frictionless ways to save,” said Cardlytics’ Chief Business Officer, Ross McNab. “As the economy continues to open and summer approaches, now is an important time for brands to take a closer look at their existing marketing strategies and determine what is really driving moments of impact and measurable incremental return on ad spend and make any adjustments accordingly.”

To learn more about Cardlytics’ solutions for driving incremental impact and the Q1 2022 State of Spend, visit https://cdlx.cc/Q12022StateofSpendPR

About Cardlytics

Cardlytics (NASDAQ: CDLX) is a digital advertising platform. We partner with financial institutions to run their rewards programs that promote customer loyalty and deepen relationships. In turn, we have a secure view into where and when consumers are spending their money. We use these insights to help marketers identify, reach, and influence likely buyers at scale, as well as measure the true sales impact of marketing campaigns. Headquartered in Atlanta, Cardlytics has offices in London, New York, Los Angeles, San Francisco, Austin, Detroit and Visakhapatnam. Learn more at www.cardlytics.com.

Purchase Intelligence Could be the Key to Helping Consumers Through the Cost-of-Living Crisis

Energy bills, food prices, national insurance, and inflation are all on the rise causing mounting financial pressures and concerns for consumers. As the cost of the weekly food shop goes through the roof and the price of filling up the car creeps, consumers are looking for better ways to manage their finances and find the best savings options possible, creating new opportunities for their banking relationships.

Our new data from a poll of over 2,000 UK consumers finds that almost three quarters (73%) plan to shop around more this year in search of the best deals. At the same time, over half (57%) are checking their banking apps more often now than they did a year ago.

While consumers are forced to juggle these new demands on their finances, it creates a valuable opportunity for banks to utilise their platforms for good, building deeper relationships and positioning themselves as a resource for help.

As banks have transitioned to online and mobile banking in recent years, the ‘face’ of banks is fading. Whilst digital banking has revolutionised the way banks can reach customers, whenever and wherever they are, it has made it increasingly difficult to build and maintain the same deep and highly personal relationships.

With inflationary pressures eating into earnings, consumers are increasingly looking to their banks for financial advice and resources. They’re particularly seeking personalised approaches that are tailored to their specific financial situations – from help with budgeting to advice on the best ways to maximise savings.

This cost-of-living crisis provides both a motivation and an opportunity for banks to reconnect with their customers. So how can they best help?

Banks have access to a wealth of purchase insights and by evaluating which brands are seeing the biggest rise in average transaction values, they can see exactly where customers are feeling cost pressures. Banks can then introduce personalized offers that can help address these, from discounts on petrol to cash back on the brands they visit the most, helping them play a key role in supporting their customers where it matters.

And it isn’t just about the positive savings impact for the consumer; there are clear benefits for the bank too.

Bank of America is one example that is truly leading the way - its Preferred Rewards Program has a clear tiered total benefits program for cross-product engagement, meaning that as a customer’s balance grows, so will the benefits a customer receives.

To realise the true value of loyalty programs, banks must adapt their mindset to view them not from the transactional lens of “purchase this and get something in return,” but from the perspective of providing support and creating a point of relevance in a customer’s life. The rising cost of living provides that sweet spot of relevancy for banks.

As the cost-of-living crisis continues to wage war on consumer’s purse strings, there’s a clear opportunity for banks to utilise the data they already have, showing their customers that they truly understand their individual financial pressures and can support them.

Rather than just powering transactions in the background, banks can – and should – utilise the purchase intelligence they have at their fingertips to play an active role in supporting consumers through the cost-of-living squeeze. The result for banks? More financially stable, engaged, and loyal customers.

<strong>Cardlytics Appoints Jose Singer as Chief Product Officer</strong>

ATLANTA, GA – April 21, 2022 – Cardlytics (NASDAQ: CDLX), an advertising platform in banks’ digital channels, today announced the appointment of Jose Singer as its Chief Product Officer.

Beginning May 16, Singer will succeed Michael Akkerman and lead Cardlytics’ overall product strategy, including the evolution and expansion of its advertising platform capabilities and user interface. He will also be closely aligned with sales and engineering leadership, striving to deliver a seamless, best-in-class product platform and go-to-market strategy that exceeds partner expectations and expands the overall adoption of Cardlytics’ solutions by advertisers.

“Jose brings a wealth of knowledge and experience in developing successful operating models that seamlessly align the product and engineering functions for optimal performance in a fast-paced industry,” said Cardlytics CEO, Lynne Laube. “We are thrilled to have him join our team at a pivotal moment in time for our company as we work to migrate to AWS alongside the rollout of a number of new platform capabilities on behalf of our partners and their shared customers.”

Singer joins Cardlytics from Nextdoor where he served as Head of Product for business and agency solutions. In this role, Singer was responsible for the end-to-end product experience, unifying the ad platforms and overall strategy for small and enterprise advertisers. Prior to his role at Nextdoor, Singer held various leadership positions at Yahoo, including Vice President of Product for their advertising solutions, running their native, search, service delivery, and supply-side ad platforms.

Singer holds a Master of Law from Columbia University and a Bachelor of Law from the Pontifical Catholic University of Rio de Janeiro in Brazil. Singer will be based in Cardlytics’ San Francisco office.

About Cardlytics

Cardlytics (NASDAQ: CDLX) is a digital advertising platform. We partner with financial institutions to run their rewards programs that promote customer loyalty and deepen relationships. In turn, we have a secure view into where and when consumers are spending their money. We use these insights to help marketers identify, reach, and influence likely buyers at scale, as well as measure the true sales impact of marketing campaigns. Headquartered in Atlanta, Cardlytics has offices in London, New York, Los Angeles, San Francisco, Austin, Detroit and Visakhapatnam. Learn more at www.cardlytics.com.

<strong>Cardlytics Announces Timing of Its First Quarter 2022 Financial Results Conference Call and Webcast</strong>

Atlanta, GA – April 19, 2022 – Cardlytics, Inc., (NASDAQ: CDLX), an advertising platform in banks’ digital channels, today announced that its first quarter ended March 31, 2022 financial results will be released on Monday, May 2, 2022, after market close. The company will host a conference call and webcast at 5:00 PM (ET) / 2:00 PM (PT) to discuss the company’s financial results.

A live audio webcast of the event will be available on the Cardlytics Investor Relations website at http://ir.cardlytics.com/.

A live dial-in will be available at (866) 385-4179 (domestic) or (210) 874-7775 (international). The conference ID number is 8338158. Shortly after the conclusion of the call, a replay of this conference call will be available through 8:00 PM ET on May 9, 2022 at (855) 859-2056 (domestic) or (404) 537-3406 (international). The replay passcode is 8338158.

About Cardlytics

Cardlytics (NASDAQ: CDLX) is a digital advertising platform. We partner with financial institutions to run their rewards programs that promote customer loyalty and deepen relationships. In turn, we have a secure view into where and when consumers are spending their money. We use these insights to help marketers identify, reach, and influence likely buyers at scale, as well as measure the true sales impact of marketing campaigns. Headquartered in Atlanta, Cardlytics has offices in London, New York, Los Angeles, San Francisco, Austin, Detroit and Visakhapatnam. Learn more at www.cardlytics.com.

Shopping is back, Baby!

In 2021, apparel retail and online sales recovered to pre-pandemic levels as previously sheltered consumers began shopping once again. Consumer spending levels recovered from a record sales plunge and gradually increased from January to April, but then had a sharp spike with the availability of vaccines. Spend then held strong throughout the remainder of the year.

With consumers returning to the store to shop, you may be surprised to learn how much they’re spending on apparel this year – Consumer spend grew to $57.8 billion up from $44 billion last year, slightly rebounding from $57.6 billion in 2019.

But what are the actual trends driving this growth?

Key Takeaways for 2021 Apparel Trends

- Despite being hit hard by the pandemic, the apparel category has surpassed 2019 spend levels

- Average basket size is the strongest contributing factor to the increase

- The branded, discount, and athleisure categories are the standouts in terms of share and sales growth

- Apparel spend is returning in-store (v. online)

Shop less, spend more

Shopping trips overall are down, and fewer consumers are buying apparel (-6.8% vs. 2019), but don’t despair, there is room for optimism! Even with fewer consumers, shoppers are buying in greater quantities. The average basket size is the strongest contributing factor to the increase in apparel sales, up 13.4% compared to 2019. It’s fair to say shoppers today are extremely valuable.

So, what are they buying?

We’ve gathered some of the top trends for the apparel industry to uncover what’s driving growth and which categories are full of opportunity for recovery:

- Branded, athleisure, and discount retailers are the real winners to date in terms of share and sales growth.

- Department stores, shoes, and children’s apparel haven’t fully rebounded to 2019 spend levels.

- The shoes and athleisure categories are attracting more new customers than all other apparel sub-categories.

Where are the spenders spending?

By now, it’s pretty clear that while consumers were stuck at home during the height of the pandemic, online shopping became increasingly popular. Even with a digitally transformed shopping experience, shoppers rediscovered the joy of shopping in-store as share of spend slowly returned to in-store channels.

The takeaway

The state of the apparel industry is never static, but the changes over the past two years have been especially dramatic. Every shift and every new trend creates another opportunity for brands to grow, but only if they can learn how to change, too.

Cardlytics allows its brand partners the opportunity to reach real people at a time when they are already thinking about their finances. In return, these consumers receive cash back on places where they already shop, or an opportunity to discover new brand to love. Partner with us to leverage insight into new apparel spending habits and increase your share of wallet amongst crucial apparel customers.

Learn how we deliver incremental return on ad spend by contacting us today to access a free advertising opportunity assessment and gain valuable insights into your customers and competitors!

The Road to Cookieless Advertising: A Timeline

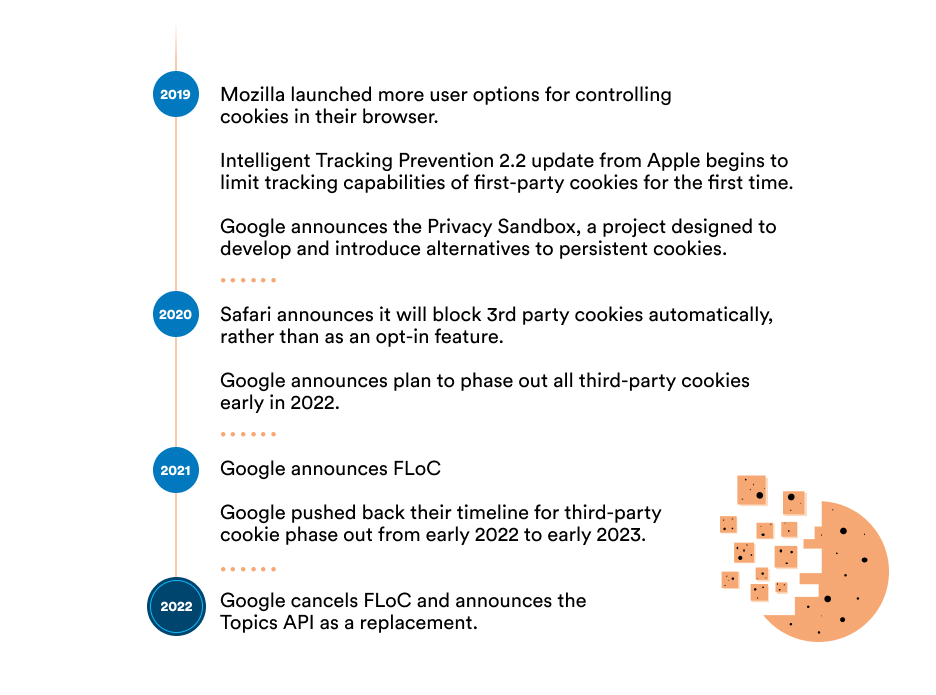

Most people don’t know the name Lou Montulli but he’s indirectly responsible for one of the biggest invasions of privacy of the modern era. In 1994, Montulli was a 23-year-old founding engineer at Netscape with a number of Internet innovations to his credit, including web browsers, HTTP proxying, and the infamous tracking cookie.

Montulli never imagined the privacy issues that would arise from the cookie. The Netscape founders were extremely privacy-focused, as were most early Internet pioneers. When Montulli created the cookie to help a single website remember a particular user from visit to visit, he believed the small text file it contained would not allow users to be tracked.

As history shows, that was definitely not the case. In record time, ad tech companies figured out how to hack the cookies and track users from site to site as they browsed the Internet.

Nearly 30 years later, ad tech has become increasingly stealthy and sophisticated in its ability to collect consumers’ most intimate personal information, often without their explicit consent. But the war between privacy advocates and the $120 billion digital advertising industry may be at an end. With Google’s latest timeline for privacy milestones, third-party cookies will disappear completely in 2023. The privacy advocates prevailed and the era of cookieless advertising has arrived.

The switch to consent-based data collection represents a significant change for consumers and advertisers alike. Although Google continues to work on third-party cookie alternatives, no viable replacement is on the immediate horizon. Given the profound implications of a cookieless future, it’s worth looking at how we got here.

How the cookie became so important

In the early days of the Internet, websites had a memory problem. They lacked a mechanism to recognize a returning user. It was a disaster from a user-experience perspective. Many of the features people take for granted today—shopping carts that remember our selections, websites that remember our login credentials and site preferences—couldn’t exist without Montulli’s cookie invention.

When advertisers figured out how to exploit cookies for revenue, the problem was more nuanced than it first appeared. At the time, advertising was the only source of revenue for most websites. Robust ecommerce was years in the future. So advertising was the only way to monetize websites and essentially keep the whole Internet in business.

The underlying exchange—free content for a limited amount of advertising—was nothing new. Radio and TV operated on a similar system. The problem was the extensive data collection and privacy implications, as you can see from the following timeline of events.

The reign of the third-party cookie

Once Google bought DoubleClick, the Internet became the wild, wild west for third-party cookies. Without regulatory oversight, ad tech companies became ever more aggressive in their data collection tactics. They went beyond online behavior and location to personal information like age, gender, income, health status, and even, in some highly unethical cases, keystrokes.

The concept of Internet privacy was dying on the vine. Despite the 2002 ePrivacy Directive requiring websites to inform users about data collection activities and allow them to opt out, many sites did not allow users to block cookies. The objective for ad tech was to collect and monetize as much detailed personal information as possible.

The tracking frenzy finally caught the attention of the Federal Trade Commission (FTC) and the European Union (EU). In 2012, the FTC slapped a record-breaking $22.5 million penalty on Google for misrepresenting their tracking activities on Apple’s Safari browser. The EU passed Directive 2109, also known as the Cookie Law, which led to the ubiquitous cookie consent popups on websites.

Big Tech also stepped up to give consumers more control over their data. Both Apple and Mozilla enabled third-party ad blocking on their browsers, and later, disabled third-party cookies altogether. Google Chrome, the leading browser, was the only holdout.

In 2008, Cardlytics launched its native ad platform. Cardlytics was a new solution to the privacy needs of the moment. Because it operated within the digital channels of major financial institutions and used first-party purchase data obtained with consent, it offered advertisers an ethical approach to targeted campaigns.

Internet privacy hits mainstream

Whether due to the flurry of legislation or the collective shock of the Cambridge Analytica scandal, in 2019, Big Tech finally stepped up to protect consumer privacy. Apple and Mozilla took the lead, giving users maximum control over cookies in their browsers. Apple’s Intelligent Tracking Prevention not only disabled third-party cookies, but it also gave users control over their first-party cookies for the first time.

Google was the last to the privacy party but it, too, is phasing out support for third-party cookies in 2023.

What’s coming in 2022 and beyond?

There’s a lot of apocalyptic messaging about the future of cookieless advertising. The Interactive Advertising Bureau projects that cookieless advertising will cost publishers $10 billion in revenue while Google estimates they’ll lose 50% to 70% of their ad revenue.

The developers at the Privacy Sandbox, Google’s initiative to replace third-party cookies with privacy-conscious alternatives, are working on a set of API solutions. Although Google’s Federated Learning of Cohorts (FLoC) was paused, other options are still on offer. Turtledove, for example, is designed to enable granular retargeting on an individual level. SPARROW will allow advertisers to create lookalike campaigns built around interests. FLEDGE will help them target specific user cohorts.

All of these are still in development, however, so their features and future functionality are uncertain.

The bad news is that 75% of marketers believe cookie deprecation will negatively impact their business, and nearly 80% haven’t tested an alternative solution. The good news is that organizations still have more than a year to develop and implement a plan before Google pulls the plug on third-party cookies in late 2023.

The future of cookieless advertising is in flux. Cardlytics offers a proven solution for precision targeting that doesn’t rely on third-party cookies. Get in touch to learn more.

Benefits of Loyalty Programs in a Cookieless World

Google may have delayed the ultimate death of the cookie, but that doesn’t mean marketers can breathe easy. Brands have relied on third-party cookies for behavioral targeting and remarketing campaigns for decades. Change won’t come easy.

There’s no plug-and-play replacement for third-party data on the horizon. Even though Google is putting the final nail in the cookie coffin, Apple and Firefox banished their use years ago. The heightened awareness around ethical data collection and privacy concerns means brands will need new ways to segment and activate their audience.

That’s where loyalty programs come in. Strong brand loyalty programs are built on first-party customer insights, and present a wealth of opportunity to grow your data assets for targeted campaigns. If a loyalty program isn’t part of your marketing strategy today, read on to find out why it should be.

The brave, new cookieless world

There’s no avoiding the fact that cookie deprecation will have a major impact on the way brands implement and manage marketing campaigns. Third-party cookies were the gateway to targeting consumers—observing the websites they visited, the products they bought, and even their interests and affiliations.

They also enabled accurate campaign measurement and attribution. Brands could track conversions to a particular ad and have deep visibility into ROAS. Cookie deprecation puts an end to reliable multi-touch attribution models.

With the fall of reliable multi-touch attribution, marketers need a way to make sure they have accurate, repeatable, and affordable ways to measure the incremental impact and return of ad spend on each channel.

Brand loyalty programs can be a treasure trove of insights

While consumers view unauthorized third-party data collection with disdain, they are typically willing to volunteer personal data for something of value. A recent YouGov poll showed that 88% of US adults would happily share personal information with brands if they received discounts, free products, or rewards in return.

That makes brand loyalty programs the perfect vehicle to collect meaningful, and accurate, customer insights at scale as part of a value exchange. Because loyalty programs are designed to cultivate repeat customers, the insights they generate can be used to enhance personalization efforts and build a better customer experience.

Of course, the pivot toward loyalty programs as a way to replace third-party data requires some agility in marketing tactics. The ‘awareness to conversion’ journey must be replaced by a ‘conversion to advocacy’ journey to maximize the program’s value. While a brand’s most loyal customers make up just 20 percent of its audience, they typically generate up to 80 percent of its revenue.

Brands can use a rewards program to build a loyalty bridge that turns their best customers into advocates. A properly designed and executed loyalty program is a powerful owned-media channel that builds engagement, grows market share, and drives sales.

Accelerating brand loyalty programs with Cardlytics

Most brands have a good grasp of who their customers are when they’re making a purchase with them, but they lose visibility once the transaction is complete. Brands have no idea, for example, what share they’re getting of a particular customer’s category spend or just how loyal their ‘loyal’ customers really are. Without that insight, they run the risk of spending money where there is no headroom.

Because Cardlytics partners with top financial institutions, we have a “whole wallet” view of consumers, with insights into how, when, and where they spend both in and out of the store. Armed with this first-party data, brands can deliver targeted offers to their most loyal customers, increasing their lifetime value. They can also re-engage lapsed customers with compelling offers designed to turn them into loyal fans, thus expanding market share.

It’s a win-win for brands and customers. Brands have more efficient use of ad spend with the same or better visibility into performance as third-party cookie campaigns. Customers get reward offers that make them feel valued, increasing their loyalty as a result.

Brands with loyalty programs are a giant leap ahead when it comes to a cookieless future. That’s because responsibly managed first-party data will become the only path for brands to grow their audience, market share, and sales once the cookie crumbles.

Get in touch to learn more about how partnering with Cardlytics can turbocharge your loyalty efforts and increase sales.

Cardlytics vs. Cookies: A privacy-safe solution

Brands have been implementing cookies to track website visitors, gather data that helps target ads to the right audiences, and improve customer experiences for years. Marketers also use cookies to learn what else customers view online when they aren't on their website.

But that'll all change dramatically, with Google planning to phase out the third-party cookie by 2023. Google's original announcement indicated that "users are demanding greater privacy—including transparency, choice, and control over how their data is used—and it's clear the web ecosystem needs to evolve to meet these increasing demands."

So, if your advertising strategy relies on third-party cookies, it's time to consider alternatives. That's where Cardlytics comes in. Let's start by looking at how Cardlytics works and why we're the privacy-safe solution.

Key takeaways:

- Learn more about Cardlytics and how it works

- An explanation of how Cardlytics is a privacy-safe solution

- Learn more about how Cardlytics is your answer to the deprecation of third-party cookies

How Cardlytics works

Engage customers through targeted advertising

Cardlytics allows you to engage customers through targeted advertising in a one-of-a-kind native ad platform. We integrate ads within online, mobile, and email channels at top financial institutions in the US and UK. And the best news is that our ads only reach verified adults who actively manage their money.

That's because bots don't have bank accounts. Our ads provide real value to customers with targeting based on past purchase history. They also act as the critical tipping point for purchase.

Measure campaign performance

We also close the loop with actual transaction data. Our team measures campaign performance, reporting online and in-store sales down to the penny. Best-in-class test versus control proves the incremental sales impact of our campaigns. Results can also be independently verified by Nielsen Sales Lift Measurement.

The power of Purchase Intelligence(™)

Finally, Cardlytics customers enjoy the power of Purchase Intelligence. We have a complete view of consumer spending through our partnerships with top banks, including purchases made with your competitors. This Purchase Intelligence is foundational to everything we do—our team helps brands like yours understand where, when, and how people buy.And the best part—these are real insights from over 170M real consumers. As a result, Cardlytics has visibility into one out of every two card swipes in the US, equating to more than $3.3T in consumer spending annually. Then, we analyze the data for Cardlytics customers to develop actionable insights.

How is Cardlytics the privacy-safe solution?

User privacy has always been a part of the Cardlytics DNA. Beginning our journey as a partner to financial institutions required an intense focus on protecting sensitive data and respecting usage limits as a trusted platform.

As we've grown and expanded our product offering, we've maintained that focus on user privacy. At the same time, our team has also found unique and respectful ways to bring the insights from our expansive dataset into the hands of Cardlytics customers.

We only see a consumer as an ID number and never receive their personally identifiable information (PII). That way, absolutely no PII is transferred between Cardlytics and our partners—it's all anonymous. And the good news is that Google's announcement does not impact how we measure, report, or use cookies for performance validation.

We also use only first-party purchase data from our partners to target and serve content within our native advertising platform. As a result, Cardlytics does not require third-party information to operate our platform. In addition, we don't make our audiences available on any other medium, making Cardlytics the privacy-safe solution.

Why 3rd party cookies are a privacy issue

While brands find 3rd party cookies beneficial when it comes to targeting audiences and increasing sales, there are privacy concerns. For example, because 3rd party cookies are hosted by an ad server, consumers can’t consent to them. That is a concern because they allow companies to track a consumer’s online behavior, thus enabling them to target them with specific goods or services.

The death of third-party cookies is coming. Mozilla Firefox and Apple Safari have already banned them, and Google says it'll block them on Chrome in 2023. That's why it's vital to rethink how you'll connect with consumers. To identify new and not-so-loyal customers now, Cardlytics provides a powerful solution because we identify opportunities for sales growth through Purchase Intelligence.

Our robust AI and dozens of analysts have insight into where and when customers buy online and in-store. Becoming a Cardlytics customer means you can answer crucial questions that inform business decisions. Our first-party purchase intelligence data remains reliable, actionable, and protected.Undoubtedly, working with Cardlytics can help you better reach the right audience with more relevant offers in a third-party cookie-free world. So, what are you waiting for? Contact us today for more information about becoming a Cardlytics customer and how we can help exponentially grow your sales.

State of Luxury Spend

The road ahead for the luxury shopping market looked a little dicey in 2020. With restrictions on both in-store shopping experiences and travel, sales plummeted by as much as 68% in some areas. As months went by and the global COVID-19 pandemic endured, nervous CEOs cautiously planned for the future of their brands.

As we look back on 2021, many voices in the industry wondered if luxury spend would recover. We now know the answer is a definite, "yes" as luxury spending for 2021 recovered and surpassed 2019's pre-pandemic numbers by 27%.

Key Takeaways:

- 2021 luxury spending recovered and exceeded 2019 levels.

- Average order value (AOV) led sales growth, supported by an increased trip count and eager customers to see some return to normalcy.

- Luxury shoppers still prefer in-person shopping experiences, despite initially embracing e-commerce at the pandemic's beginning.

- High-frequency customers drive the majority of luxury sales.

A rough 2020 leads to an astounding 2021

Luxury retail industry trends have been up and down–hitting rock bottom in March 2020 with a 68% drop as a global pandemic gripped the fears of shoppers around the world. And on top of that downturn, we watched stores temporarily close, and shoppers become reluctant to visit those stores that were open.

We also saw an abrupt halt to international travel, accounting for up to one-third of all luxury sales. Global travelers enjoy the allure of buying authentic luxury where it's made, so it felt like the luxury shopping industry would become strategically dismantled.

Some shoppers were giving luxury online shopping a try, but the industry outlook was bleak. Low retail sales left luxury brands buried in extra inventory–a problem that disproportionately hurts luxury brands. The fundamentals of supply and demand illustrate that when inventory is high, pricing is low.

Luxury brands rely on exclusivity, so typical retail tactics like steep discounts only work to devalue the brand. These brands knew the road would get bumpy; they braced for the worst but came out of the pandemic pleasantly surprised.

Luxury spending saw the first signs of recovery in June 2020, when the data began trending upward. Progress was slow at first, and both retailers and luxury brands anxiously watched as trip counts and average order volume steadily rose.

By the end 2021, cushioned by a healthier holiday spending season, luxury spend trends outperformed even the most optimistic predictions with $2.2B in growth. Luxury retail trends are showing promise for a strong and stable recovery, but it hasn't been equally distributed.

Luxury markets are prone to polarization. Luxury shopping is about authenticity, status, and self-esteem. Some brands–and products, are simply better at filling that need for consumers.

AOV tells the story

So, were consumers compensating for their feelings of pandemic-driven isolation and fear in 2021, or is this genuine growth? The story is in the data. Let's look at the factors contributing to the unexpected boom in luxury spending habits.

Cardlytics' first-party data identified average order volume (AOV) as the largest driver of increased spending. This means that shoppers were simply buying more on each shopping trip. There was also a notable increase in customer trips in 2021 compared to data from 2019, which supported the AOV-led growth.

A deep dive into the data shows luxury spending statistics on AOV took a nose-dive in the first two weeks of the COVID-19 pandemic. The average sale dropped from $308 to $175. And, at the lowest point, it dropped to $167 in May of 2020 before beginning a slow climb towards recovery. By the holiday shopping season, AOV was up–way up. By the end of 2021, the annual average had reached $350 per trip.

While e-commerce has been a big driver of change in other markets, luxury shopping was less affected before the pandemic. The in-store experience plays a pivotal role in what brings shoppers to luxury brands. The smell and touch of authentic, high-quality leather can't be replicated in a digital environment–at least not yet.

And a big part of the self-esteem boost that shoppers receive comes from being pampered by personal shoppers while strolling across shiny marble floors.

Luxury retail saw a spike in online shopping when mandates and public health concerns forced the hand of consumers, but it was temporary appeasement. As restrictions eased, shoppers returned to the stores in droves, craving that luxury shopping experience.

The data shows that the mix of shoppers in the store and online is about the same for 2021 as it was before the pandemic; let's take a look:

- 2019 Spending Mix: 57% in-store and 43% online.

- 2020 Spending Mix: 47% in-store and 53% online.

- 2021 Spending Mix: 57% in-store and 43% online.

While the mix shifted back in favor of in-person shopping, the volume of online sales for luxury brands is still significant. The digital age provides a valuable opportunity to connect with new consumers differently.

As we look towards the next year, online sales are anticipated to grow–leaving luxury brands with dual commitments to extend the same level of luxury service both in-person and online.

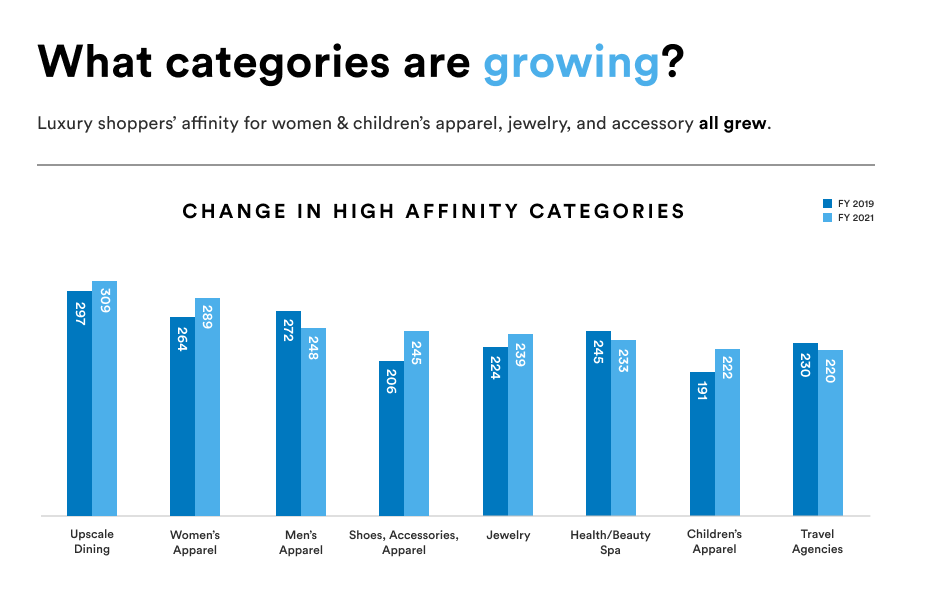

Must-Have Luxury Goods with the Most Growth in 2021

Luxury retail performance can be unpredictable even in a strong market because brand affinity has always been tied to public perception. A new era of socially-conscious consumers is now more powerful than ever before in determining which brands are in–and which ones are out. This provides some insight into luxury spending growth in 2021.

As surprised as many luxury brands were by this growth, many are eager to know where consumer spending is increasing. The top-performing categories included women's and children's apparel, jewelry, and accessories. Across the retail industry, luxury and value brands saw the most growth in 2021, attracting renewed interest and inviting disruption from new competitors.

For one, Amazon has entered the market in big ways–first, they opened their Common Threads storefronts to showcase the work of individual designers, and then they launched a luxury brands mobile app exclusively for Prime members.

Previously untouchable brand opportunities are back on the market, and like-it-or-not, the luxury retail sector is embracing new ways to connect with customers in a digital world.

The luxury shopping market is evolving

Two more critical pieces of data that will shape the future of luxury retail trends are consumer base and loyalty. Overall, the number of luxury shoppers has increased 2% since 2019. It seems that more consumers are craving authentic experiences that only luxury brands can deliver.However, there's a catch–a new generation of consumers are showing less brand loyalty overall. They're not just looking for a brand name—consumers are looking for values alignment and are willing to shop where they can get what they want.

As much as 65% of customers making multiple luxury purchases are shopping with two or more different brands. This means that quality and reputation only go so far–even in the luxury goods market. Brands face more pressure to cultivate and maintain customer relationships as we move beyond the pandemic.

What to expect in 2022

Luxury brands can expect to see trends in continued growth. Data-driven predictions on consumer spend are modeling an anticipated growth of 25% compared to 2019, outperforming non-luxury sectors by as much as five times the growth.

There will always be a strong market for bargain hunters and value-minded shoppers, but only the luxury retail market is forecasted with significant growth for the coming year.

The market is ripe with opportunity for brands that are able to keep pace with consumer needs and remain relevant in a changing world. Modern shoppers expect the convenience of omnichannel accessibility–interacting with brands when and how they choose.

Shoppers demand values alignment on important issues like sustainability and inclusivity. And at the same time, they expect the same level of luxe quality goods and services that define the luxury shopping experience.

From technology to social responsibility, luxury brands have more on their plate than ever before. The good news is, Cardlytics can help. Learn about how we can provide you with invaluable data-driven insights to help shape your marketing strategy and align your brand for growth.

Get our insights delivered to you

Stay up to date. Subscribe now.